Blog Details

Positive vs Negative GEX: How Dealer Positioning Shapes Price - Flowtopia

Price action is not driven by sentiment alone. In index products and heavily traded single names, dealer hedging often plays a direct role in whether volatility gets absorbed or amplified. That is why positive vs negative GEX matters. The question is whether the current options structure is likely to make price more stable, more fragile, or more explosive once a move starts.

For traders, one of the most useful ways to separate noise from structure is to understand positive gamma vs negative gamma. It gives context for hedging structure, helps explain why some breakout attempts die immediately while others expand, and makes gamma-based trade planning more practical when it is combined with flow, open interest, and actual price behavior. That same context-first approach matters here: gamma should help frame market behavior, not replace judgment.

What GEX is really measuring

Gamma exposure is an estimate of how sensitive dealer hedging may become as the underlying moves through an options-heavy area. Flowtopia explains it as the cumulative gamma risk embedded across open options positions, especially around strikes where positioning is concentrated. When price approaches those areas, market makers may need to adjust hedges more actively in the underlying, which can affect short-term liquidity and volatility.

That matters because gamma is not just theoretical. It can change the character of the tape. When hedging is concentrated and stabilizing, the market often feels sticky and rotational, which can frustrate momentum traders. When hedging becomes unstable, price can move faster, liquidity can feel thinner, and overextension becomes more likely. The phrase positive vs negative GEX is really shorthand for those two different environments.

Why the sign matters more than the number alone

A large raw GEX figure can sound impressive, but the sign often tells the more useful story. When net gamma is positive, dealer hedging tends to lean against price movement. When net gamma is negative, dealer hedging tends to move with price and amplify it. Most serious GEX frameworks make the same point: the real value is not directional prediction, but understanding the likely quality of movement and volatility regime.

How positive gamma vs negative gamma changes the tape

The easiest way to think about the distinction is through dealer hedging behavior. When dealers are effectively long gamma, they tend to sell into strength and buy into weakness to stay hedged. That behavior dampens movement. When dealers are effectively short gamma, they tend to buy as price rises and sell as price falls, which can reinforce the move rather than slow it.

In practice, the tape usually behaves very differently in each regime:

- Positive gamma usually compresses intraday range, encourages mean reversion, and makes breakout continuation harder.

- Negative gamma usually expands intraday range, increases the odds of directional follow-through, and makes failed positioning more dangerous.

- Near-flip conditions can be messy because the market is close to shifting from one hedging regime to the other.

These tendencies matter, but they should never be treated as certainty. Flowtopia is careful on this point in its educational material: gamma exposure is contextual, not predictive in isolation. A trader who treats GEX as a complete signal will usually overreach. A trader who uses it as a structural filter will usually make better decisions.

What positive GEX often feels like

A positive gamma environment tends to produce more failed breakouts, more chop around key strikes, and more snapback behavior after short bursts away from value. Traders often get trapped here by chasing strength that looks clean for a few minutes but quickly stalls. It just ran into an environment where hedging flow worked against expansion.

GEX is most useful when it is read alongside real-time flow, historical flow, and contract-level analysis rather than on its own. If you can see supportive price structure, but your gamma backdrop is still stabilizing, you should generally expect slower follow-through and demand stronger confirmation. See Flowtopia’s GEX overview and real-time options flow guide for that broader workflow.

What negative GEX often feels like

A negative gamma environment tends to feel less forgiving. Breakouts can stretch farther than expected. Reversals can become disorderly. Small imbalances can cascade because the hedging response is moving in the same direction as price. Once price moves into an area where hedging becomes procyclical, the market can stop behaving like a range and start behaving like a fast auction.

At that point, options structure stops being theoretical and becomes directly useful. If dealers are likely to add fuel to a move, the same chart pattern can behave very differently than it would in a pinned session. This does not turn every downside move into a crash or every upside break into a squeeze, but it does increase the odds of extension and raises the cost of fading momentum.

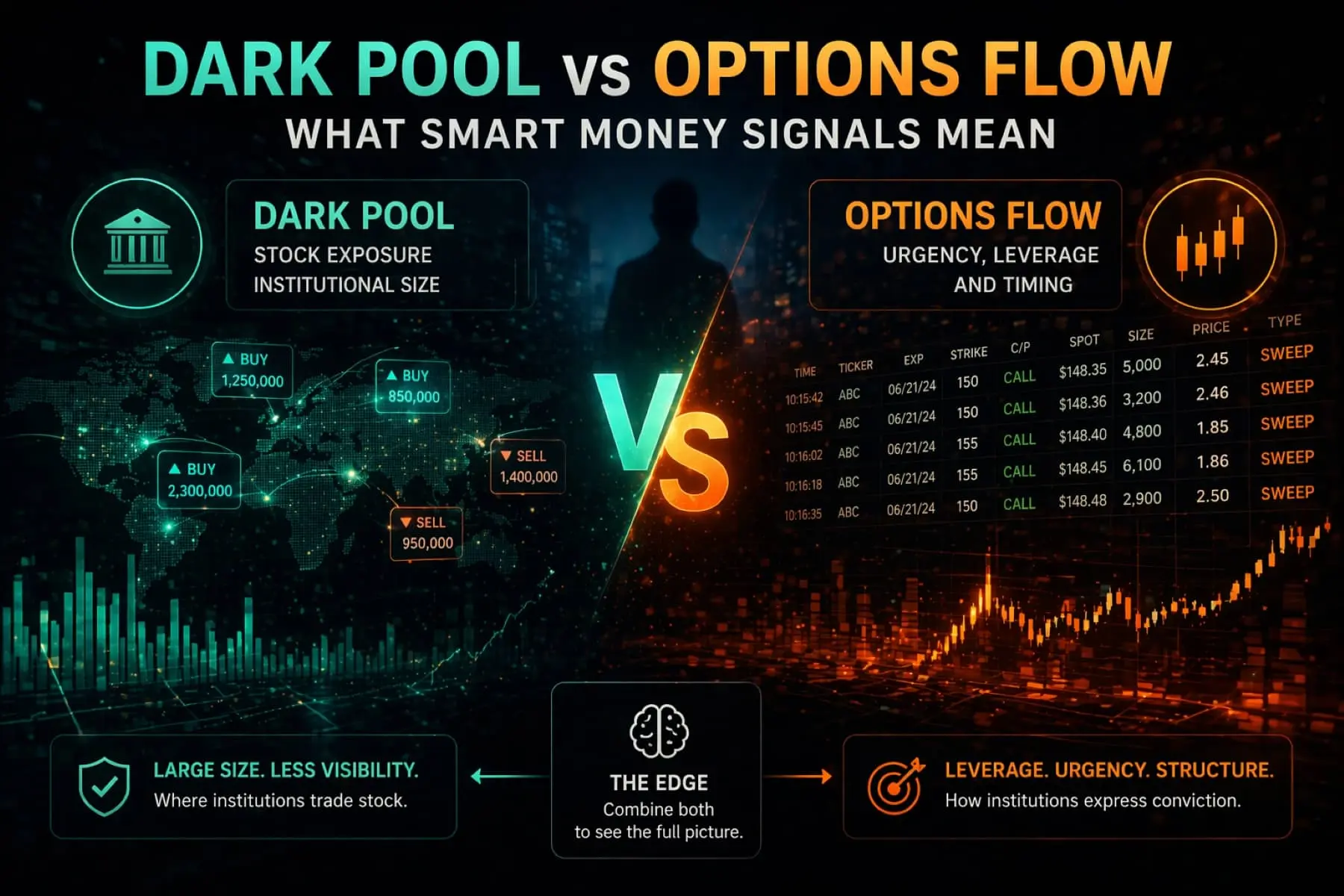

Why positive vs negative GEX should be read with flow, not in isolation

On its own, a gamma map tells you where structure may matter. It does not tell you whether fresh participation is building there, whether the aggressive side is committed, or whether the move is already exhausted. That is where options flow becomes valuable.

The strongest read usually comes from combining structural context with actual trade behavior. That means pairing GEX with repeated sweeps, execution quality, open interest context, and premium concentration. The open interest and volume guide is particularly relevant here because a contract can look active without actually representing meaningful new positioning.

A cleaner decision process often looks like this:

- Start with the current gamma regime and note whether positive vs negative GEX argues for mean reversion or expansion.

- Check whether flow is confirming that regime through repeated activity, ask-side aggression, or clear premium concentration.

- Compare the contract activity with open interest, timing, and nearby catalysts before deciding whether the move deserves conviction.

That is a far more reliable way to approach gamma exposure trading than treating one GEX number as a signal by itself. It forces you to ask whether structure and participation are aligned.

A realistic example

Imagine an index trading just below a major call-heavy area after a quiet first hour. Net gamma is positive and price keeps probing higher without holding the breakout. At the same time, the tape shows scattered call buying, but not much repeated urgency. In that situation, the cleaner read is probably caution. The structure argues for reversion, and the flow is not forceful enough to overwhelm it.

Now change the setup. The same index opens below a well-watched flip area, net gamma is negative, and within twenty minutes you see repeated ask-side call sweeps with volume expanding far beyond the prior open-interest base. That does not guarantee upside continuation, but the environment is far more supportive of it. The difference comes from the interaction between existing positioning and fresh participation.

Where traders misuse positive vs negative GEX

The biggest mistake is turning GEX into a directional opinion. GEX is usually better at explaining how price may behave after it starts moving than telling you which way it must go. Gamma exposure should be treated as contextual information rather than a guaranteed predictor, and that is the right posture.

A few misuse patterns show up again and again:

- Traders assume negative gamma automatically means trend day, even when flow is weak or mixed.

- Traders fade every rally in positive gamma without noticing that a catalyst or concentrated buying is overwhelming the stabilizing effect.

- Traders talk about positive vs negative GEX without checking where price actually sits relative to the flip or the heaviest strikes.

Another mistake is trying to force gamma exposure trading into market conditions where it is not the main driver. Some sessions are driven more by macro headlines, liquidity shocks, or sector-specific catalysts than by clean options structure. GEX still matters in those moments, but it may matter less than traders want it to. Use it to sharpen scenario planning, not to create false certainty.

What to watch instead of oversimplifying

If you want GEX to improve your process, focus on the questions it helps answer. Is the market likely to pin or expand? Are breakout attempts more likely to fail quickly or gain traction? Is the move happening near a heavy strike, a call wall, a put wall, or a flip level? And most important: is live flow confirming the structural read, or fighting it?

Those questions are what keep the framework practical and stop it from becoming oversimplified market lore. The brand language across the site consistently positions the tools as a way to interpret institutional activity more clearly, not as a shortcut around analysis.

What traders should take from dealer positioning

If gamma is positive, expect the market to resist expansion until proven otherwise. If gamma is negative, respect the possibility that the move can travel farther and faster than the chart alone implies. Then check whether the flow, open interest context, and execution agree.

That is why positive vs negative GEX should be part of a decision framework, not treated like a stand-alone answer. It helps you identify the kind of market you are trading before you decide how aggressive to be. It also gives dealer positioning a real purpose: not as jargon, but as a way to explain why price sometimes sticks to strikes and other times tears straight through them.

For traders building a more disciplined read on structure, positive gamma vs negative gamma is most useful when it is paired with the rest of the evidence. Used that way, gamma exposure trading becomes a practical framework. It helps traders judge when hedging pressure is likely to suppress movement, when it may amplify it, and when the market is close enough to a regime shift that extra caution is warranted. Flowtopia’s GEX, flow, and historical tools are built around that kind of context-driven workflow, giving traders a cleaner way to track these relationships in real time.

Similar Blog You

May Like

Understand how institutional money moves and turn complex options data into clear, actionable insights in real time.

Join traders using real-time options flow, institutional data, and advanced tools to make faster, more informed decisions.