Blog Details

What is GEX? Understanding Gamma Exposure for Traders - Flowtopia

Short-term market moves are often influenced by more than price charts alone, and one of the most important forces behind that structure is the options market. In recent years, derivatives markets, especially options, have become increasingly important for understanding short-term market behavior.

Many retail traders still rely mostly on price charts and technical indicators when trying to understand market behavior. However, these tools may not always capture the structural forces operating behind the scenes.

Institutional investors and professional traders often study derivatives positioning because options markets can show where capital is concentrated across strike prices and expiration dates.

Over the past decade, options trading activity has grown substantially. According to the Options Clearing Corporation (OCC), U.S. options markets have frequently averaged more than 40 million contracts traded per day. During periods of high market volatility, this number has occasionally exceeded 60 million contracts in a single trading session.

As options activity expands, more traders are looking at frameworks that explain how options positioning may influence market behavior.

One concept that has gained considerable attention among derivatives traders is Gamma Exposure (GEX).

Gamma exposure refers to the total gamma risk associated with open options positions in the market. When large options positions accumulate near certain strike prices, market makers who facilitate these trades may adjust their hedging positions as the underlying asset price moves.

These adjustments can sometimes influence short-term liquidity conditions and market volatility.

Traders who understand gamma exposure may interpret market behavior more clearly than traders who rely only on traditional indicators. However, gamma exposure should generally be viewed as contextual information rather than a guaranteed predictor of price direction.

How Gamma Exposure (GEX) Works

To understand the meaning of GEX in trading, it helps to start with how options pricing works.

Options contracts give traders the right, but not the obligation, to buy or sell an asset at a predetermined price before they expire. Because options pricing depends on several variables, traders often analyze options positions using mathematical sensitivities known as the Greeks.

One of the most important Greeks is gamma.

Gamma measures how quickly an option’s delta changes as the underlying asset price moves. Delta itself represents how sensitive an option’s price is to movements in the underlying asset.

How Market Makers Hedge Gamma Exposure

When many options contracts exist near the current market price, gamma exposure may become concentrated around those strike levels.

In practical terms, options gamma exposure reflects the cumulative gamma risk across open options contracts in the market.

Market makers who provide liquidity in the options market typically hedge their exposure in the underlying asset. As the price of the underlying security moves, market makers may adjust their hedging positions by buying or selling shares.

These hedging adjustments can sometimes influence trading activity in the underlying market.

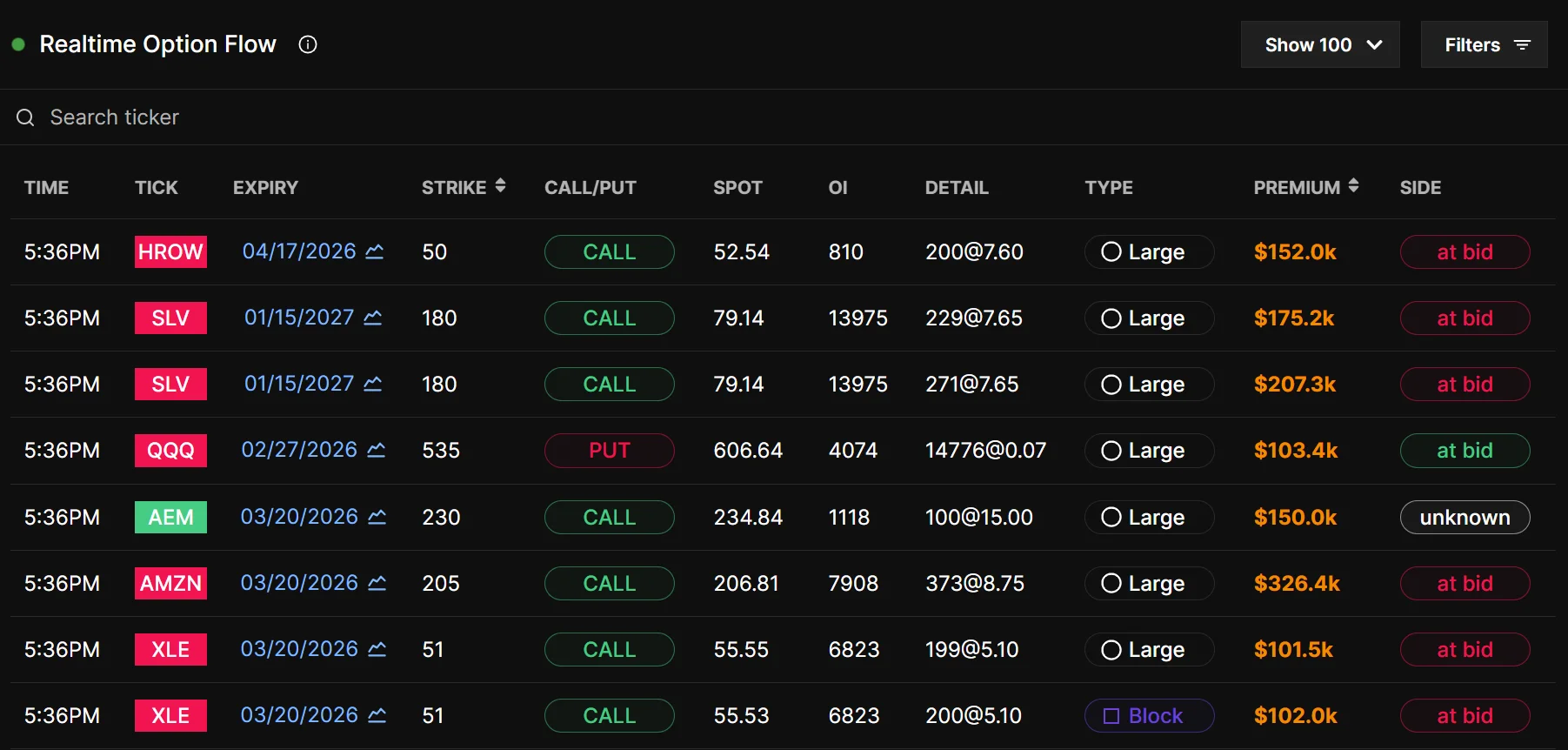

Traders who study derivatives positioning often analyze gamma exposure alongside tools that track unusual options activity and institutional order flow. One of the most useful analytics tools for identifying institutional trading patterns is options flow, which helps traders understand where large market participants may be deploying capital.

Gamma Hedging and Market Liquidity

Options markets include several types of participants, ranging from retail traders to hedge funds, institutional investors, and market makers. Market makers play a central role by providing liquidity for options trades.

However, market makers typically aim to avoid large directional exposure.

To manage risk, they frequently hedge their options positions using the underlying asset. This hedging process is closely connected to gamma exposure.

When prices move closer to heavily traded strike prices, market makers may need to adjust their hedging positions more frequently.

Key Factors That Influence Gamma Exposure

Several factors influence how gamma exposure develops across the market:

- the total open interest across strike prices

- the concentration of contracts near the current market price

- changes in implied volatility and time to expiration

- institutional positioning in call and put options

Taken together, these factors can influence how hedging activity shifts as prices move through the market.

Because of this, some traders monitor gamma exposure to identify price levels where liquidity conditions might shift. It is important to emphasize that gamma exposure does not guarantee specific price outcomes. Instead, it represents a structural feature of the options market that may influence price behavior under certain conditions.

Why Gamma Exposure Matters for Traders

As derivatives markets have expanded, options positioning has become an important area of analysis for many traders.

Institutional investors frequently use options for hedging, speculation, and portfolio risk management. As a result, options markets can sometimes reveal where large concentrations of capital are positioned.

When traders ask about gamma exposure, they are usually trying to understand how options positioning might influence market behavior.

Market Dynamics Influenced by Gamma Exposure

In certain conditions, gamma exposure may coincide with several observable market dynamics:

- price stabilization near heavily traded strike levels

- increased volatility during rapid market moves

- liquidity shifts when market makers adjust hedging positions

For example, when a large number of options contracts are concentrated around a specific strike price, that level may sometimes act as a temporary area of price stabilization.

However, these effects depend on many variables, including liquidity conditions, macroeconomic developments, and investor sentiment. Traders can explore institutional analytics tools to better understand how these dynamics are monitored across options markets.

Gamma Walls and Gamma Flip Levels

Within options market analysis, traders sometimes refer to concepts such as gamma walls and gamma flip levels.

A gamma wall generally refers to a strike price where a large concentration of options contracts exists. Because market makers may hedge around these levels, some traders believe they can occasionally influence short-term price behavior.

For example, if a large number of call options exist at a particular strike price, hedging adjustments may occur as prices approach that level.

Understanding Gamma Flip Levels

A gamma flip level refers to a point where the overall gamma exposure in the market shifts from positive to negative.

Some traders monitor these levels because they believe the market environment may behave differently depending on whether gamma exposure is positive or negative.

However, the interpretation of these levels remains subject to debate, and they should not be viewed as definitive trading signals.

Real Example of Gamma Exposure in Market Behavior

Gamma exposure attracted significant attention during the 2021 meme stock rally, particularly in stocks such as GameStop.

During several trading sessions in early 2021, options trading activity surged dramatically as traders purchased large volumes of call options.

According to exchange data, GameStop options volume temporarily exceeded several million contracts in a single session, far above its historical average.

Some analysts suggested that this surge in call option demand contributed to a phenomenon often described as a gamma squeeze.

In simplified terms, as the stock price increased, market makers hedging these call options may have needed to buy additional shares of the underlying stock.

This additional demand may have contributed to further upward price movement.

However, it is important to recognize that several factors influenced these events, including retail trading activity, liquidity conditions, and broader market sentiment.

Gamma exposure alone does not fully explain such price behavior.

Limitations of Gamma Exposure Analysis

Although gamma exposure has become widely discussed among derivatives traders, it also has several limitations.

Options markets involve complex strategies including spreads, hedging transactions, and multi-leg trades. These strategies may not always reflect directional expectations.

Despite its usefulness, several factors may limit the reliability of gamma exposure analysis:

- large options trades may represent hedging activity rather than speculation

- modeling assumptions can influence gamma exposure calculations

- sudden volatility changes may alter hedging behavior

Because of these limitations, gamma exposure should generally be interpreted as contextual information rather than a definitive trading signal.

Traders seeking deeper insight into derivatives positioning often explore analytics platforms that aggregate options data and visualize institutional activity across markets. https://flowtopia.co/

Conclusion

As derivatives markets grow, understanding how options positioning interacts with price action has become increasingly important for traders.

Gamma Exposure (GEX) is one framework traders use to interpret how options market dynamics may influence short-term liquidity and volatility.

By examining how options contracts are distributed across strike prices and expiration dates, analysts can estimate where hedging adjustments might occur as prices move.

Although gamma exposure does not provide guaranteed predictions, it can offer insight into the structural forces that shape modern financial markets.

For traders who want to understand how derivatives positioning interacts with market behavior, studying Gamma Exposure (GEX) may offer a clearer view of how institutional activity can influence price movement.

Similar Blog You

May Like

Understand how institutional money moves and turn complex options data into clear, actionable insights in real time.

Join traders using real-time options flow, institutional data, and advanced tools to make faster, more informed decisions.